Ever since the beginnings of the large-scale commercial use of wind energy in the 1990s, the industry has observed one considerable trend which remains steady to the present day: turbine growth. Recently, this trend has experienced another boost. In this article, we offer a number of explanations for this trend and discuss possible consequences.

Differentiation between onshore and offshore

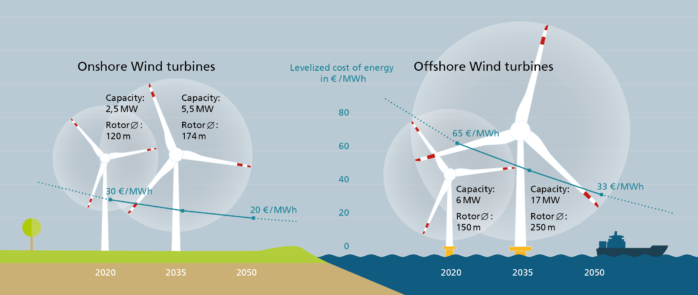

The onshore and offshore markets have been developing at different speeds for some 10 to 15 years now. Offshore turbines have been specifically designed for their purpose since the introduction of the 5 to 6 MW class. Growth in the same environment accelerated from this point onward and diameters way above 200 m are currently in the testing phase.

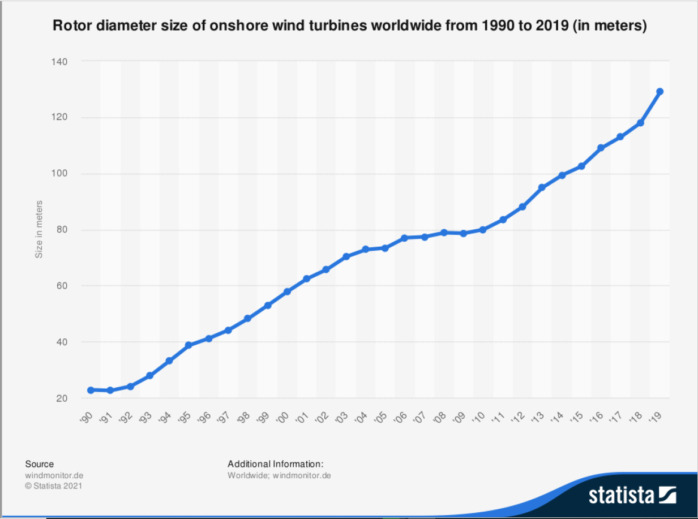

The development of onshore turbines unfolded more slowly but followed the same path, with a particular focus on a very low specific rating down to 200 watts per square meter (W/m2), making the turbines more suitable for low-wind sites, which allows projects to be brought closer to load centers and the existing grid infrastructure. Standard sizes for European markets now have rotor diameters ranging from 150 to 160 m and a 4 to 6 MW generator capacity.

Motivation and regional differences

Although the upscaling foresees a rotor weight increase with approximately the third power of the blade, which also implies increasing costs per MW installed, this does not halt the trend. For offshore turbines, when the installation, infrastructure, logistics, and O&M are factored in, it is clear that larger machines will result in a lower levelized cost of energy (LCOE) and, even if the costs per kWh increase, including for onshore projects, site or noise limitations might lead to a better return on investment (ROI) per project due to the increased total energy production.

On a turbine level, contrary to the trend of the scaling laws, some benefits can be identified when moving to larger sizes. In particular, everything related to turbine “intelligence” requires more or less the same effort irrespective of the size of the machine. Therefore, sensors, controls, and certain aspects of power electronics are becoming cheaper in relative terms for these giants.

Upscaling within or beyond current technical limits

Whereas “smaller” turbines in the range of 2 to 3 MW are still essentially being designed and manufactured within the standard engineering processes also used in other industries, e.g., shipbuilding, the larger models are rapidly moving out of this comfort zone. This increases the effort needed to set up suitable facilities (with new machinery and molds, increased transport and crane capacities), which are only required for very specific components and often only for one customer. Thus, the investment risks are getting bigger, leading to a much lower number of actors interested in this type of business.

Main technical challenges

Depending on the specific component, the new technical challenges vary slightly, but nearly always consist of a combination of size-dependent material property knowledge, fatigue issues, manufacturing capacity issues, and transport or other related challenges.

Blades rank relatively high on the list of concerns. The huge increase in length is combined with a substantial lack of material models capable of describing the long-term behavior of the composite and the very classic manufacturing process which still includes substantial amounts of manual labor.

Towers for onshore turbines in particular are facing related issues: the new tower heights required for the large rotors can no longer be realized with standard steel solutions. Hybrid approaches with a combination of concrete and steel need to support extreme fatigue loads. This loading scenario is again far outside the standard application zone of concrete and requires intensive investigations into all aspects of material behavior and its interaction with the manufacturing process – either with prefabricated elements or on-site casting.

Bearings, especially pitch bearings, are relatively new additions to the list of critical components. However, the new dimensions of up to 6 m in diameter in an application with relatively soft support structures and new loading scenarios due to the advanced control schemes create an environment which is way beyond the classic application.

Consequences for the design process

The more the design of very large machines expands beyond current engineering experience levels, the more basic research is necessary to provide the required models for material and system behavior. This is closely linked to a comprehensive validation effort, covering all areas of the famous V-model from material development to complete design verification. Given the size of the specimen to be tested, this is a tremendously expensive exercise. Luckily, another trend comes in offering a certain relief: digitalization. Digital twins and virtual testing can complement or even partly replace costly real-life testing activities and, in general, can improve the reliability of verification efforts. Still the risk remains high – erroneous design decisions are extremely expensive and difficult to correct, plus, especially in the case of very large components, all decisions are based on very little experience.

Outlook

Given the huge costs of new platform developments – both onshore and offshore – the number of players in the OEM field will most likely be further consolidated. Both extremely broad and extremely in-depth expertise is needed to push the limits of engineering and the manufacturing challenges, plus the validation effort will limit the number of actors in this industry, even with some market growth expected in the years to come. Furthermore, the field of O&M may become even more closely tied to the equipment manufacturer due to their control of critical technologies and component sourcing (and long-term service and warranty agreements). Ultimately, turbine growth also means a lower number of bigger turbines – for commodity parts in particular this could accelerate a certain level of standardization as a possible solution to compensate for lower volumes and still allow for cost reduction in this area.

Very large turbines also tend to be very smart. This could, as a side effect, allow easier integration of new features such as additional power plant characteristics, hydrogen production interfaces, etc., thereby improving the competitive edge in the system integration field compared to other renewable energy sources with little extra effort. Specific advanced technologies such as superconducting generators only come into play for sizes way beyond 10 MW. This opens up a completely new field for drastically improved designs, once again leading to further cost reductions or a broader range of applications, an assumption supported, for example, by studies from Berkely Lab.